10

Why I Hate Budgets—and What I’m Trying Instead

Financial Freedom Account Status: $315.02

Do I really need a budget? I hate, hate, hate budgets. Hate them. I’ve never thought they made sense or were realistic.

(And I’m not the only one who hates budgeting. I found at least three articles about budgeting with the word “hate” in the title.)

In my mind, budgets don’t hold up to the real world. After all, what happens when your car breaks down and you have to get it fixed? Or your cat needs an emergency trip to the vet? What then? The budget goes out the window.

And the first module in the Khan Academy financial literacy class I’m taking is about budgeting! Ugh! Apparently, budgeting is Step 1 for achieving financial literacy.

My Khan Academy class recommends the 50/30/20 rule: 50% for necessities, 30% for discretionary wants, 20% for savings.

Do I know what those numbers are for me? No, I do not.

Y’all, I just cannot figure this budgeting thing out right now. I feel like it’s so terribly complicated. And really overwhelming. And I’m already overwhelmed with life, with trying to pay my bills on time, with a literal fascist about to take office in my country…

I’m kinda freaking out, if I’m being honest.

Bottom line (for now): I am not going to commit to a budgeting method. However, as a first baby step, I am going to track my money. All the money in, and all the money out.

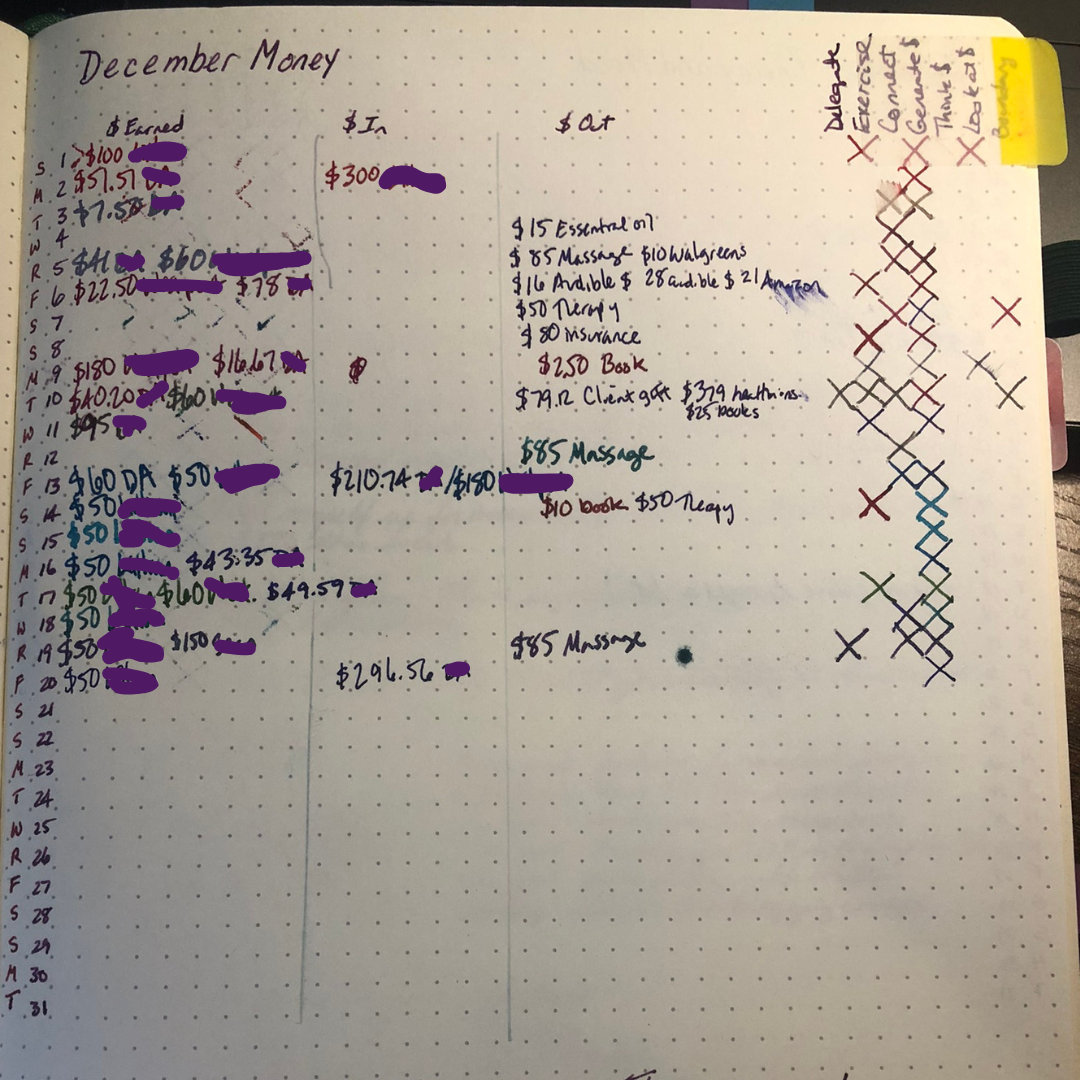

I’ve already been tracking my money in and money out on my bullet journal.

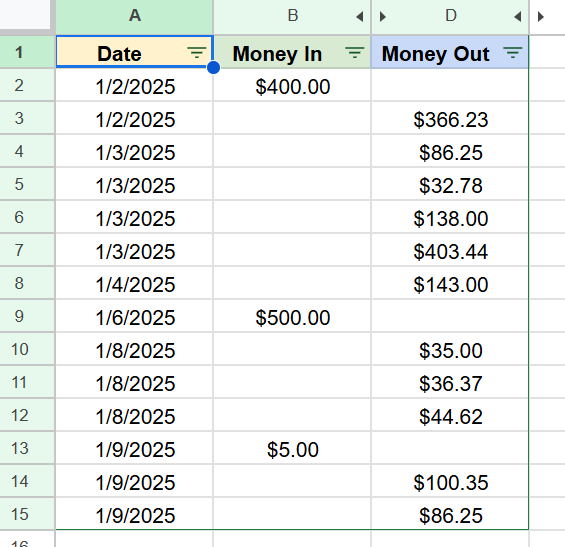

But now I commit to tracking it more completely and with more intentionality. Since we just started 2025, it seems like an opportune time to get started. Here’s my spreadsheet so far.

Once again, I am accountable to you. I’ll report back once the month is complete.

What are your thoughts on budgets? Do you keep one? Do you hate them?